Beyond another set of disappointing economic prints, a major repricing of China’s risk premium followed the release of China’s regulation plan through 2025. This plan puts the emphasis on national security, data privacy, social impact (targeting inequalities and a worsening demography), monopolies, innovation, and foreign entities. It suggests that regulatory pressure, that already hit dozens of companies for several months, is here to stay and to broaden to multiple sectors.Xi Jinping’s speech on "Common Prosperity" was also consistent with prospects of a deep revamping of the business environment. At the cost of international investments, authorities are willing to shape up innovation complex in strategic areas and ensure better social cohesion through a more sustainable economy, both under their tight control. In other words, authorities might seek to reform their ranks at home to prepare for tomorrow’s big clashes abroad. In the process, foreign companies exposed to China might face eroding revenues and margins. Through higher taxes and greater regulatory constraints large Chinese companies would be hit too, as well as their suppliers. Furthermore, a period of higher macro uncertainties in China looks probable, at least until authorities feel they have gathered enough control and made enough progress.

Like most investors, managers within Lyxor’s peer group were caught off guards. They navigated the turmoil but did not meaningfully beat their benchmark. Those deploying neutral or active trading strategies generally outperformed. The bulk of their losses came from their long positions, mitigated by gains on their shorts. Managers had already reduced their net exposures before the summer and were not the biggest sellers. While remaining positioned on the consumer recovery theme, they sold stocks most vulnerable to regulatory pressures and credit tightening, especially within the tech, financials, and real estate sectors, as well as foreign stocks exposed to China. They remained broadly neutral on factors.

Positive alpha in Q1 was eaten away in Q2 over the range-trading phase. Managers then added limited alpha during the summer. They see persisting volatile conditions but opportunities from healthier valuations and technicals. They added call options. Meanwhile, the equity environment is undergoing profound changes, calling for a remodeling of risk management.

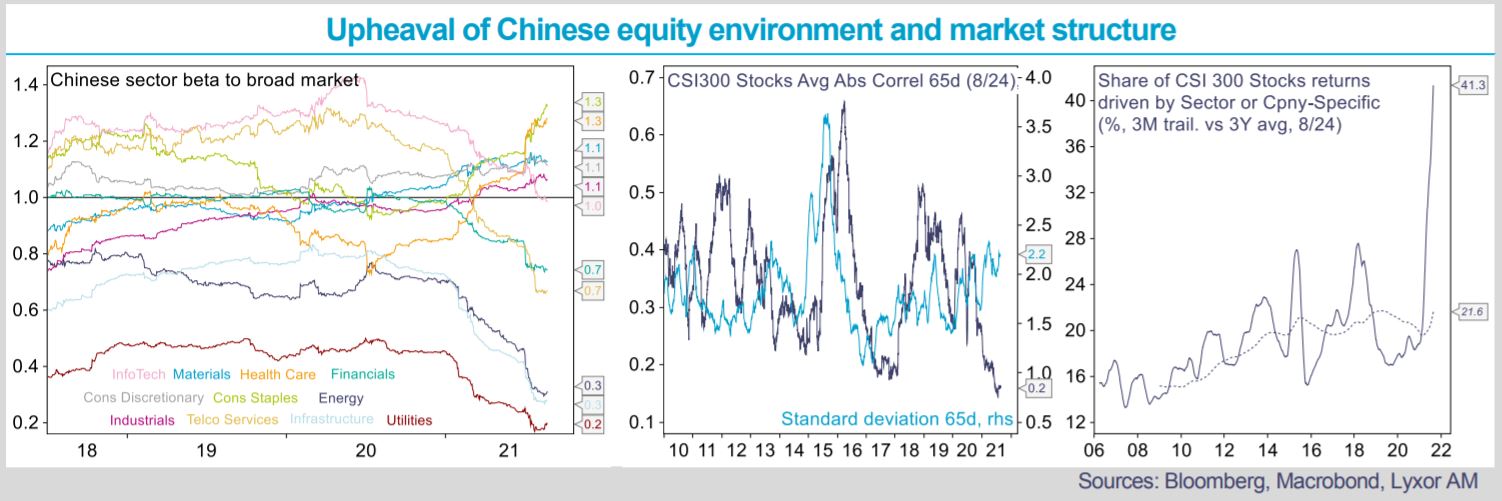

Stock correlations keep on falling while return dispersion rises. Stocks are increasingly driven by idiosyncratic factors and

sector sensitivities to broad markets were reshuffled (healthcare has become cyclical unlike the energy sector now behaving

like a defensive). While theoretically favorable to alpha, these changes are largely driven by speculative public interventions,

which might prove in practice challenging to exploit by managers, at least until dust starts to settle down.