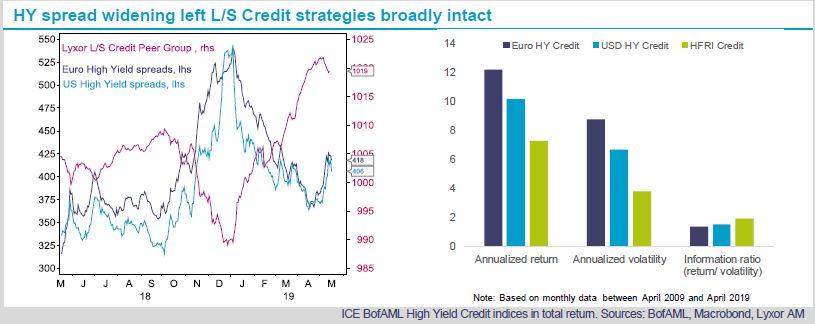

In a context where rising trade uncertainties have interrupted the rally in risk assets, L/S Credit strategies have been resilient in May so far. Such resiliency took place despite a widening in High Yield (HY) credit spreads, by approximately +35bps both in Euro and in USD. The Lyxor L/S Credit Peer Group was down -0.2% month-to-date, while the Global Peer group was down -0.7%. Based on a sample of 30 L/S Credit UCITS strategies, the best performing one month-to-date was up +0.6% and the worst performing one was down -2.0%. Since the beginning of 2019, L/S Credit strategies outperformed, up +3.0%.

Our views on the strategy have been constructive over recent months, assuming that i) sovereign bond yields are low and will likely stay low for longer as monetary policy will not normalize anytime soon; ii) carry strategies such as HY Credit should benefit from the portfolio rebalancing effect, whereby low bond yields on safe long-term securities compress risk premia for lower graded securities; and iii) L/S Credit strategies should benefit from the compression in risk premia while controlling for volatility. We estimate that L/S Credit strategies halved the volatility in returns of HY Credit over the past ten years (see chart below). We also estimate that the information ratio of L/S Credit has been close to 2, significantly above the ratio for both Euro and USD HY during the same period (1.5).

The remaining hedge fund strategies were slightly down month-to-date. CTA, Global Macro and L/S Equity are down roughly -1% month-to-date. On a positive note, L/S Equity Market Neutral has also been resilient and appears to be in a better shape after disappointing returns over the past six months. The strategy has historically been sensitive to the momentum risk factor in equities and it turns out that after the strong performance of low beta stocks during the recent quarters, the momentum risk factor is less tech-driven and reflects more the performance of low-beta stocks. We stay nonetheless relatively defensive on the strategy although we think that the worse is behind us.

Going forward, we believe that market conditions remain vulnerable. After the year-to-date rally in risk assets, the trade war escalation between the U.S. and China is a valid reason to take profits and reduce risk in portfolios. We also believe that both countries will eventually find an agreement, but such agreement could take place after intense market pressure.