The country has found it difficult to implement reforms, particularly to its notoriously rigid labor market, and faces growing anti-EU sentiment as austerity measures bite. But France has many things in its favor, not least a highly favorable demographic trend that will set it apart from Germany in the decades to come, he says. “France is widely seen as the sick man of Europe, but this is an exaggeration,” says Cornelissen. “There’s a lot of pessimism about France inside and outside the country – what the French call morosité. Certainly the rest of Europe is a bit disappointed with the reform drive of the current French government.”

“France has a highly inflexible labor market and there is a worry also that it lacks competitiveness. In the past, France had significant industrial giants and made quality products, but the worry now is that standards are getting lower, in autos for example. And France is still pretty expensive.”

Sitting out problems

Cornelissen says France’s Socialist President François Hollande resembles the former German Chancellor Helmut Kohl, who was famous for his tendency of trying to sit out problems. “Hollande is also sitting out the economic problems, and hoping that the cyclical recovery will save the French economy, and him. So that’s worrying other European partners who would like to see a more reform-minded government.”

“Usually, one country has to be the laggard in Europe, but a rising tide will eventually lift all boats, including the French one. What had dampened growth is the lack of investment by the government, and austerity is also hitting the French economy. However, the latest GDP figures showed government consumption and investment rising again. We also need the private sector to invest more in France, and perhaps we’ll see that with the ongoing recovery.”

“And the weakening of the euro will help French competitiveness. The French Mirage fighter is popular again, particularly in the Middle East, so perhaps we shouldn’t worry too much.”

‘The weakening of the euro will help French competitiveness’

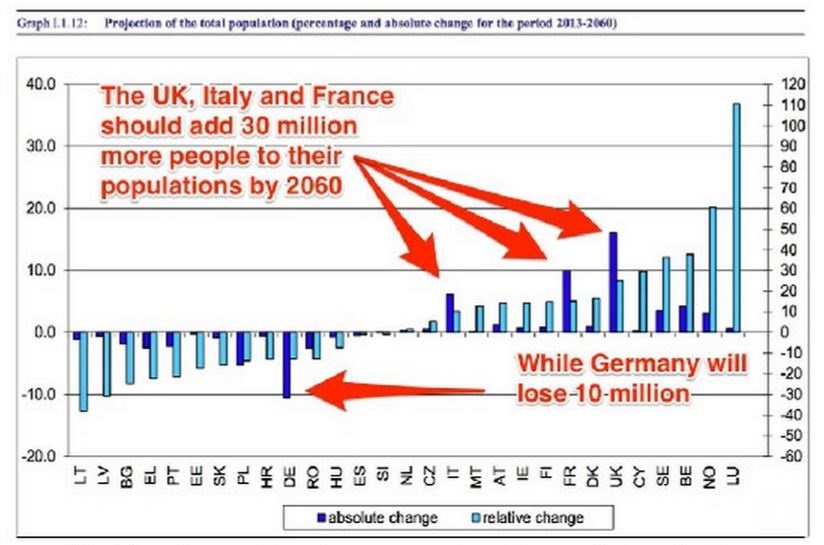

Demographics a major advantage

Cornelissen says the main thing in France’s favor is its growing population. “France has an interesting development in that it has better demographics than most other countries in Europe. If current trends continue, at some point France will have more inhabitants that Germany. France’s population is rising, naturally and through immigration, with about 2% annual population growth, while Germany’s population is shrinking.”

He says the chief political worry is the rise of the euro-skeptic French National Front, led by Marine Le Pen, who has become increasingly popular on the back of anti-immigration policies.

“Hollande may face Marine Le Pen in a presidential election, but it is highly unlikely that she will ever become President of France, especially now with the recovery going on in Europe,” says Cornelissen.” As the Eurozone recovers, the popularity of the euro-skeptic parties will decrease.”

Indeed, some critics allege that France gets too much of a smooth ride within the EU, and is allowed to bend rules over deficit reduction and austerity measures. France has long deployed the infamous ‘l’exception Française’, where it signs up to commonly agree policies and then exempts itself, but it is just too important to the Eurozone to be treated harshly, says Cornelissen.

“There is a lot of ‘hoo haar’ that the French receive special treatment within the EU – it keeps getting leeway on its public deficit targets,” he says. “But now that we have a pro-business French government, it would make no sense to put extra pressure on the country with more austerity targets. So it is sensible politics.”

‘There is a lot of ‘hoo haar’ that the French receive special treatment within the EU’

Debt is under control

He says French debt and deficit figures are not particularly alarming. “The French deficit is 3.8% of GDP, and central government debt is above 96%, which is a bit on the high side, but the creditworthiness of France is no problem. This is reflected in the market, because the bond spread between France and Germany is very low.”

“And there is an implicit risk premium here which is very low, because Germany will never let France go. The two counties lie at the very heart of the EU; France is essential for its existence. So the German government will always be reluctant to openly criticize France: it will always handle France with care.”

Robeco is overweight on French stocks, owning Axa, LVMH, Rexel, Société Générale and Total, among others. “France has some well-run high-quality companies which are interesting to investors,” says Cornelissen. “Generally we have been a bit cautious on European shares because a lot of good news has been priced in, but this has nothing to do with France and its fundamentals.”

“Indeed, there is a slight yield pick-up vis-a-vis Germany, so French bonds are seen as a ‘higher-yielding core Europe’, which is the right political and economic diagnosis I would say.”