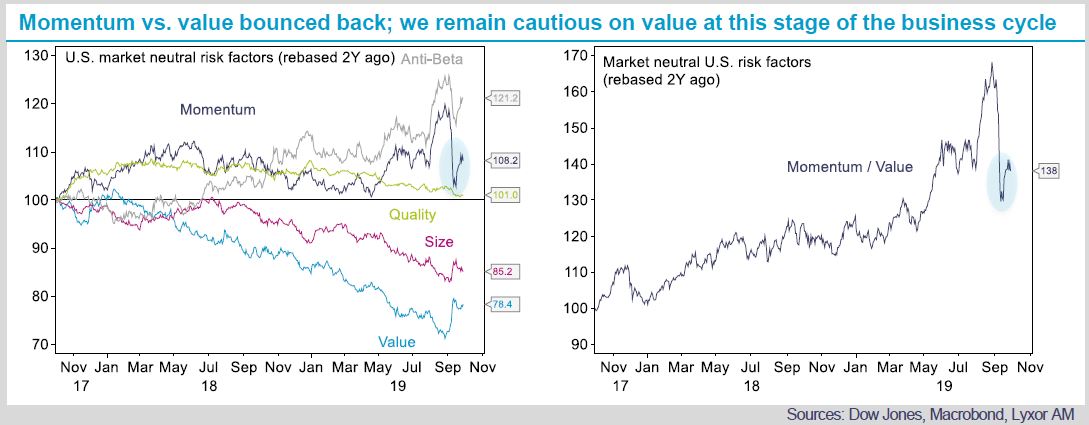

Renewed optimism on the U.S. economy in recent weeks was fueled by the resiliency of household consumption and better than expected factory output. As a result, bond yields rose from very depressed levels during the first half of September, which translated into a sharp reversal in momentum stocks to the benefit of value ones. In the space of alternative strategies, the rise in bond yields penalized CTAs (-3.0% month-to-date) while the momentum reversal detracted from Market Neutral L/S Equity performance (-0.1% month-to-date). The remaining alternative strategies were up, with Global Macro outperforming (+1.5% month-to-date).

As of end-September, the rise in bond yields and the sector rotation in equities appears to be behind us. Both CTAs and Market Neutral L/S Equity strategies rebounded last week (+1.6% and +0.2% respectively). As expected, the rebound in value stocks was short lived and we remain cautious on this risk factor at this stage of the business cycle. Yet, there are some signals that a cyclical upturn could take shape in the U.S. We believe a manufacturing recovery is nonetheless contingent on reaching a trade truce between the U.S. and China and the next two weeks will be critical in that regard. The U.S. administration is planning to hike trade tariffs on USD 250bn of imports from China on October 15th, but the stance has turned more conciliatory in recent days. If such tariff hike does not take place, there is room for optimism, which may translate into additional pressure on momentum vs. value stocks. But we believe the probability of a trade resolution in Q4-19 is low. Hence, we expect the bounce back in momentum stocks to continue.

Going forward, our stance remains defensive on equities, in particular on European, Japanese and EM markets (UW). In the space of alternative strategies, we prefer Market Neutral L/S vs. Directional L/S, despite the fact that the latter has adopted a cautious stance in portfolios and was quite resilient in August. As discussed on page 2 of this report, Market Neutral L/S have a long bias towards momentum stocks and should benefit in relative terms if our expectation that the bounce back in momentum stocks will continue. Finally, we stay constructive directional L/S Credit strategies in a low bond yield environment which is likely to last.