These fees are far from being insignificant for investor returns

Hedge funds often charge variable management fees in addition to a fixed management fee, both paid on an annual basis. Typically, the most common cost structure is the format 2% - 20% (fixed - variable).

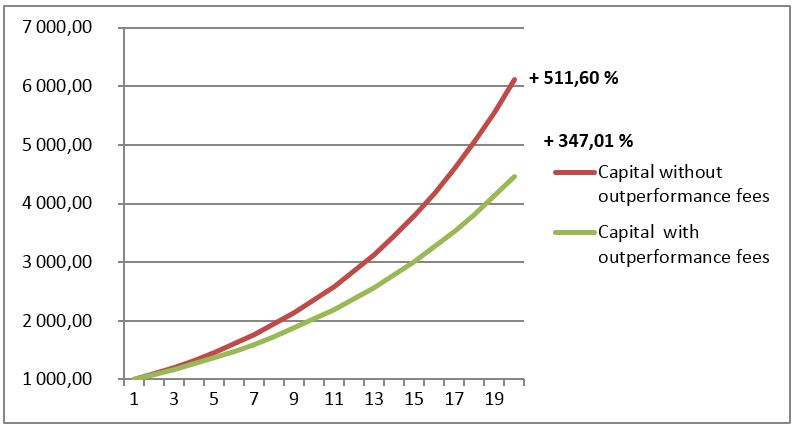

Obviously variable fees are only levied if returns are above a hurdle rate. Libor is generally used as a reference rate. These fees are far from being insignificant over a long period of time as shown in the graph below. However, to better meet customer needs, "in recent years, more and more hedge fund managers, especially in the United States, have decided to offer products without any performance fees; a trend that should gradually take place in Europe" according to Duncan Wilkinson, CEO of Alpha Simplex.

Return impact over 20 years

Hypothesis : Initial investment (1 000 €) over 20 years, given a 10 % annualized rate of return (20 % performance fees, 1 % risk free rate).

Hypothesis : Initial investment (1 000 €) over 20 years, given a 10 % annualized rate of return (20 % performance fees, 1 % risk free rate).

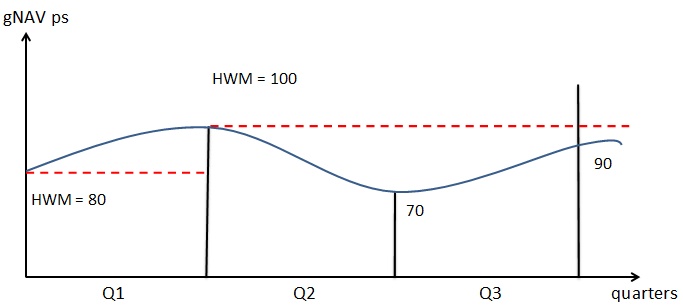

However, it is important to note that performance fee calculation includes thresholds or "high-water marks" (HWM) which means that this fee is only applicable when the net asset value (NAV) of the fund exceeds its highest level recorded in the past. As a result, investors avoid to pay commissions during periods of underperformance.

For example, if a fund experiences a period of underperformance during the second or the third quarter of a given calendar year (cf chart on the below), investors would not pay a commission fee until the NAV reaches again the value from the Q1 i.e 100.

Source : Finaquant

Source : Finaquant

This is a reason that may explain why hedge fund managers recording heavy losses, prefer sometimes to close their fund to order to open a new one; a HWM too far away from the current NAV gives them little hope to collect variable fees in the near future.