Diversified investors will find some comfort as bonds yields stabilized. In the medium-term, we stay constructive and argue that U.S. equities offer entry points at current levels.

Hedge fund performance was flat last week (from October 10th – October 17th) and L/S Equity strategies outperformed according to liquid benchmarks. The strategy captured the rebound that others, such as CTAs, did not because of systematic deleveraging. Broader measures of performance also point to L/S Equity outperformance year-to-date (up to end-September) versus an overall industry benchmark.

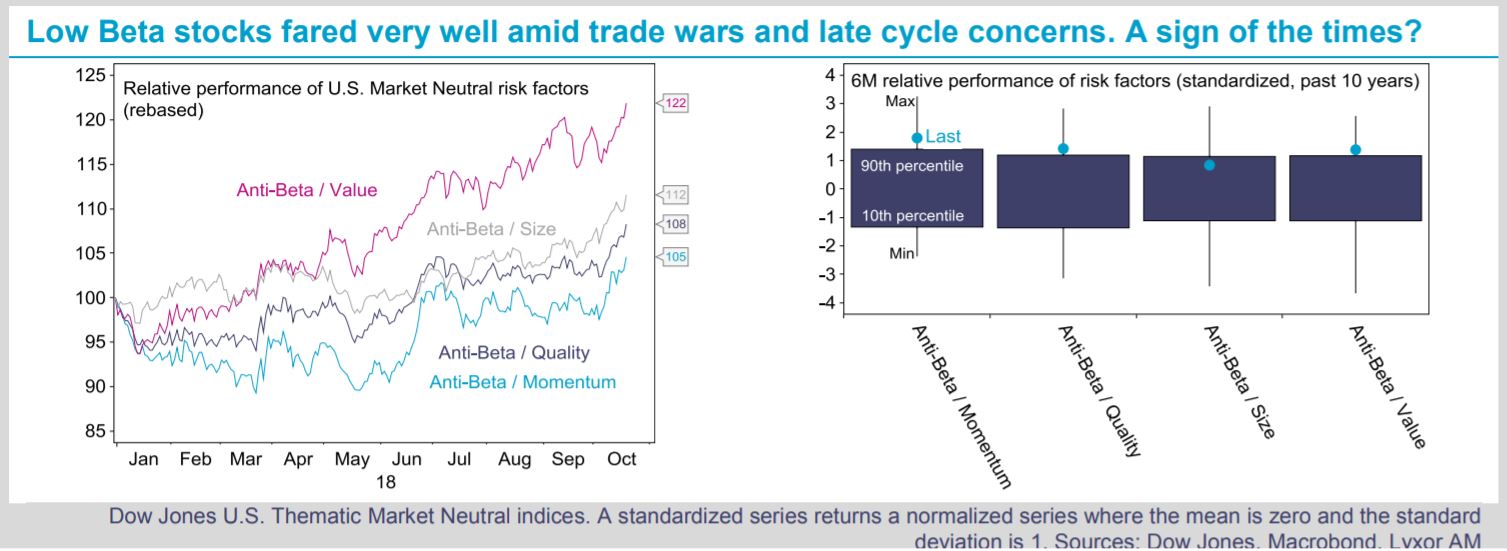

Yet, it has been a difficult year for L/S Equity strategies so far. Alpha generation has lagged most prior years amid risk factor rotations which saw low beta stocks outperforming. Recently, value stocks also staged a rebound and momentum stocks were under pressure. From a regional perspective, U.S. L/S Equity strategies faced difficulties due to their bias towards growth/ momentum stocks which suffered lately. European L/S strategies fared better as they have lower style biases and lower net exposure than U.S. peers. Market Neutral L/S strategies fared slightly better month-to-date but, at the difference of diversified L/S Equity strategies (i.e. non-market neutral), they did not rebound since the trough.

Going forward, a few remarks deserve attention regarding equity risk factors. First, we do not believe in a sustainable rebound of value stocks at this stage of the economic cycle. Second, we still believe in growth/technology stocks on the back of the assumption that bond yields have limited upside room from here. Third low beta stocks make a lot of sense at this stage of the business cycle where U.S. overheating fears may give way to recession fears in the coming months. When such views are applied to L/S Equity strategies, they suggest a preference for variable biased strategies that can adjust their net exposure down or up quickly.

Investors should also favor strategies that are tactical and less biased towards risk factors.