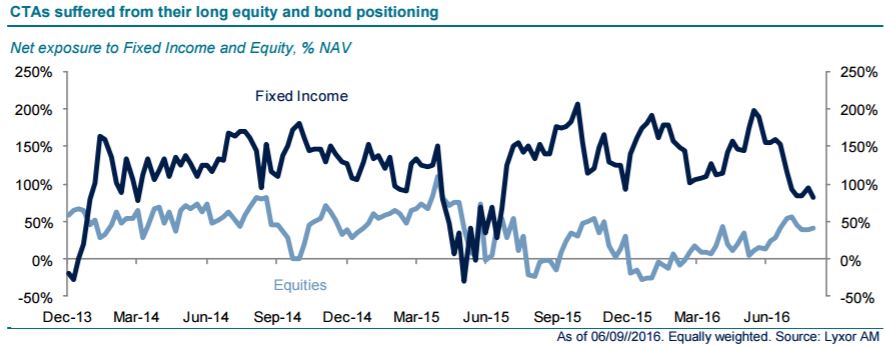

The drawdown on equities and bonds, an unusual positive correlation, has caused losses on risk parity and CTA funds. The latter experienced a drawdown that is comparable with previous episodes of jumping correlations in Q2-13 and Q2-15. L/S Equity funds were also down last week, though market neutral players were flat to slightly positive.

On a positive note, Event-Driven managers were flat in the aggregate while merger arbitrageurs were positive. Event-Driven is now the best performing strategy in 2016 YTD.

Meanwhile, Global Macro managers outperformed on the back of their short duration stance and long USD positions. Overall, hedge funds were down 0.8% last week, a rather mild movement compared to the 2.6% loss registered on the MSCI world and the 1.6% loss registered on the 10-year Treasury (performance between Sept. 6th and Sept. 13th of total return indices).

While we believe that the Fed is unlikely to hike rates at its Sept. 21st FOMC meeting, any hawkish stance is likely to lengthen the bond market correction. Since 2010, bond markets experienced three major corrections: in 2010, in 2013 (the taper tantrum) and in 2015.

On average, the 10-year Treasury lost 7% during these periods and the sell off lasted for 44 days from peak to trough. As shown on page 2, recent bond market movements are, thus, comparatively mild. But on top of the FOMC meeting, the recent rise of Donald Trump in US presidential polls and Hillary Clinton’s health issues contributed to raise uncertainty.

Trump’s election campaign entails expansionary fiscal policies which could exacerbate bond vigilantes’ concerns in case he continues to catch up in polls.

As a result, we tactically cut the investment recommendation on long term CTAs to neutral (from slight overweight) and upgrade short term CTAs to slight overweight (from neutral).