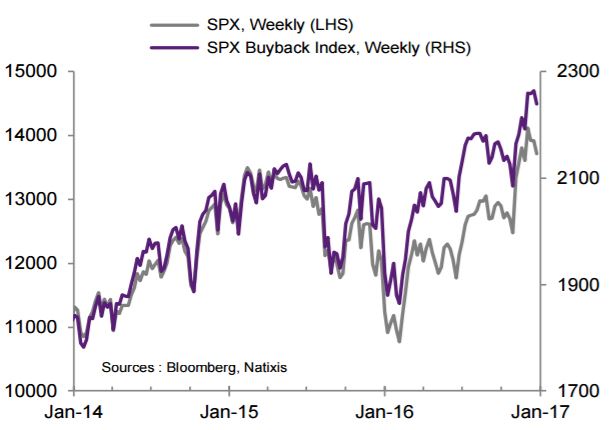

S&P 500 Buyback Index, which has hit the highest in late 2014/early 2015, had retreated outperformance during most of 2016. With Donald Trump’s victory in November, however, buyback indices and buyback related ETFs again hit the market higher. S&P 500 Buy Back Index, which tracks 100 companies with highest buy back activities in the S&P 500 list, has risen from the lows of 2016 after the election and currently is traded at the record highs (Chart 1).

Chart 1. S&P 500 Buyback Index vs S&P 500 Index

The overperformance of buyback related index in the last weeks is closely link to the expectation by markets of (i) a lower federal corporate tax rates and (ii) the prospect of repatriation of foreign profits that could be used to buyback stocks. The president elect has offered to lower the tax rate from 35% to 15% while the House of representatives (HR) wants to lower it to 20%. As for foreign profits, D. Trump offered a “deemed repatriation” plan at a rate of 10% [1] while the HR offered a mandatory repatriation tax rate of 8.75% for profits held in cash and 3.5% for profits that has been permanently reinvested.

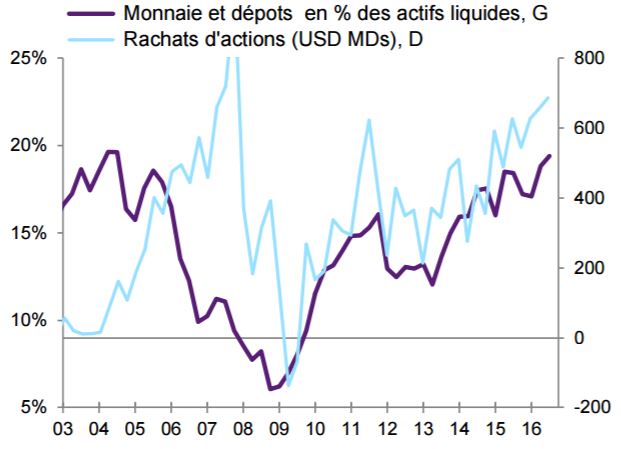

Lowering the corporate tax rate to 15% or even 20% would surely boost corporate operating cash flows. If we look at 2004 as a reference point, corporates brought back approximately 45% of their foreign profits. According to the Joint Committee on Taxation there is roughly $2.6 trillion of profits held offshore today. Therefore a wild guess would be that corporate could bring as much as $1 trillion. Yet, we need to emphasize that in 2004 corporates brought back their profits on a voluntary basis and at a lower tax rate (5.25%). Furthermore it is hard to tell how much of today’s foreign profit is held in cash (the part that has been permanently invested will not come back). Despite uncertainties on much these policy changes will boost operating corporate cash flow, the impact on buyback (chart 2) is likely to be substantial.

Chart 2: US Non-Financial corp. Liquid assets and share buybacks

(Quarterly Flows, BN)

We believe that the likely fiscal changes mentioned above will create favorable environment for US companies for share buybacks for two reasons:

1- It has been widely argued that when they brought back their profits in 2004, corporates used the cash to do share buybacks.

2- Distribution of revenue via share buybacks has been a greater channel than via dividends in the US since 2000 and its share has been growing

continuously (chart 3). In addition, corporates have been dedicating a larger share of their cash flow to shareholder payouts.

3-The shares of companies with higher buyback activities have done well due to growing earnings, which in turn led them to generate the surplus cash to be used to fund …more buybacks.

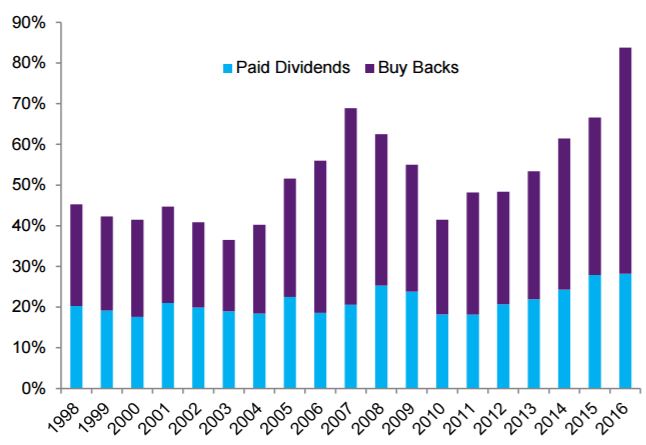

Chart 3 : S&P 500: Dividends and Buy Backs