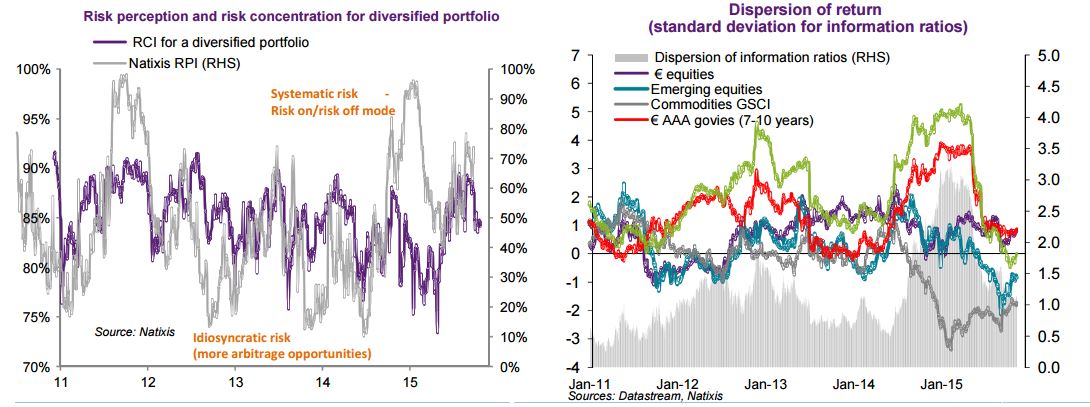

The risk concentration index (RCI [1]) for a diversified portfolio had been on a downtrend since the start of 2014. The latest risk aversion spell has brought this to an end. This index, which measures the diversity of risk sources, peaked when markets were mainly guided by the perception of the Chinese risk and by the re-emergence of a systematic risk.

This evolution reflects a tarrying up in the sources of diversification, as underlined by the information indices for the different asset classes in recent months.

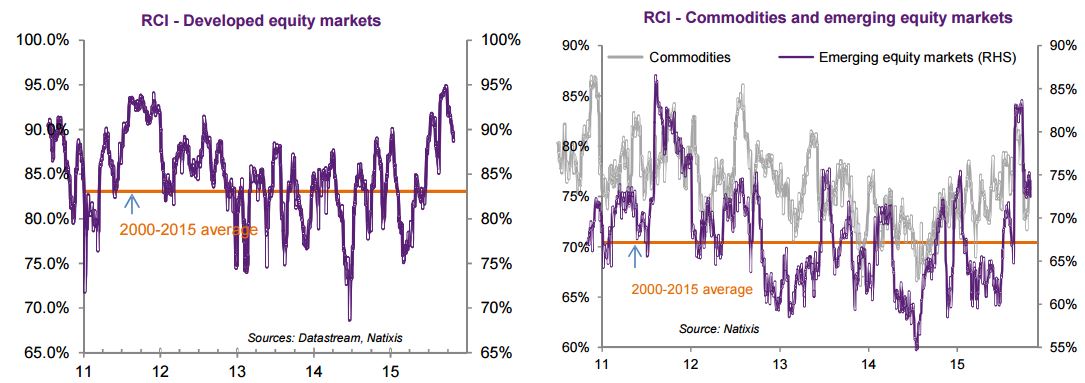

Regarding more particularly the equity market, the degree of concentration reached a particularly high level in August in both developed and emerging countries.

Since then, a downtrend has set in and looks set to continue in coming months. The divergence in the economic cycles and in monetary policies within developed economies, more than ever in evidence, should see the degree of concentration in developed equity markets decline to much lower levels, much as observed at the end of 2014 and the start of 2015.

The return to more moderate levels of risk concentration has been even swifter in recent weeks in the case of emerging equities. The recent decline of the RPI for the commodity markets is not foreign to this development, highlighting a finer differentiation in the case of commodity-exporting emerging economies.

The context is much as it was at the end of 2014 and start of 2015 and should be characterised by a reduction in risk concentration between assets classes and between assets of the same class (geographical arbitrages), while the idiosyncratic risk (in evidence before China caused the market to switch back to risk off mode) should stage a comeback.