This week was uneventful for most hedge fund strategies amid low trading volumes, few market catalysts and limited changes in risk assets’ prices. The Lyxor Hedge Fund index was flat. Merger Arbitrage and Global Macro funds were the two exceptions.

The former outperformed on Pfizer beating out Sanofi in the take-over of Medivation in the oncology segment. Several managers were already positioned for a bidding war on this company.

By contrast, Macro funds’ shorts on U.S. bonds and longs on USD temporarily played out adversely. Shifting perceptions on the timing of the Fed’s next rate hike ahead of the central bankers’ annual Jackson Hole meeting generated some volatility in rates and currencies. Expectations on further easing programs from the ECB and the BoJ were also mildly revised down.

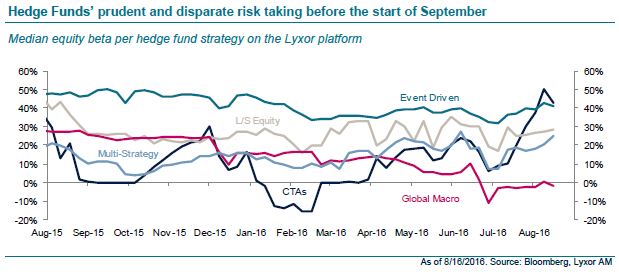

Hedge Funds modestly increased risk over the course of the summer, though heterogeneously across strategies. While September seasonality has statistically been supportive for risk assets, hedge funds remain conservatively positioned.

The lack of decisive market trends and uncertainty about the mood of investors as they head back from their summer break will not last indefinitely. Market movers will quickly reemerge as we head into September.

The tone from Jackson Hole, the U.S. jobs report, and the big three meetings (ECB, BoJ and Fed) will be closely monitored. Additionally, the G20 summit, key Chinese economic releases, and the first U.S. presidential debate at the end of September are on the radar. They are likely to generate more trading opportunities for hedge funds.