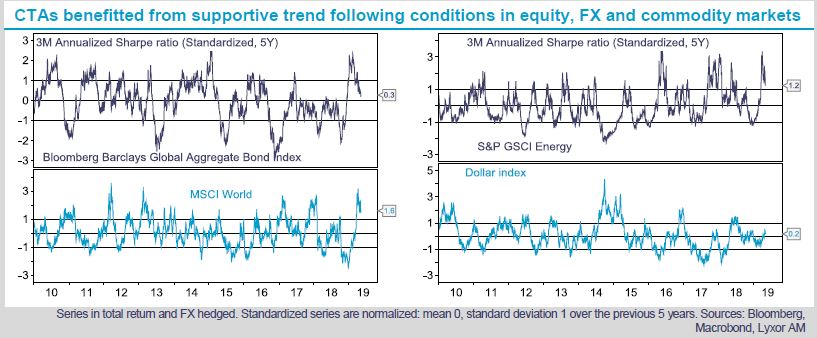

In April, CTAs benefitted from the robust performance of equity markets, as well as from the rebound of the U.S. Dollar Index and energy prices. CTAs’ short positions on agricultural commodities were also rewarding. The overall positioning has recently evolved in favor of equities vs. bonds, though CTAs maintain long positions on both asset classes. Long exposures to energy contracts and the U.S. Dollar were also reinforced.

Meanwhile, systematic Global Macro strategies, a subset of our Global Macro peer group, also outperformed both in April and year-to-date (2.3% and 3.9%, respectively). Systematic alternative strategies are on a winning streak at present, but investors remain indifferent. Flow data from eVestment suggests the pace of net outflows from CTA strategies has not eased (-5.6bn USD in Q1-2019, following -19.3bn USD in 2018). Academic research has explored the momentum risk factor, but systematic strategies are broader (though they tend to have varying degrees of sensitivity to the momentum risk factor). According to Daniel and Moskowitz1 “momentum crashes […] occur in panic states, following market declines and when market volatility is high, and are contemporaneous with market rebounds”. At first glance it looks like the probability of a momentum crash is currently low, but investors will probably need more evidence of solid and persistent positive returns to reconsider the strategy.

Our views on CTAs stay neutral, which means that we recommend a 10-15% allocation to CTAs in a hedge fund portfolio over the next 6 to 12 months.

Despite the poor performance of CTAs in 2018, investors should keep in mind that over the past 20 years CTAs outperformed equities with: i) a low correlation to global stock indices; ii) a lower volatility in returns (8% vs. 14%); and iii) a lower maximum drawdown (23% vs. 55%). Based on historical evidence, the strategy deserves to be reconsidered in our view.