Problem #1: Normalizing Policy

The Fed’s first (and most obvious) problem is one of economics: How do you normalize monetary conditions without derailing the economy? This is central banking 101. Without belaboring the point, the Fed (and at some point the Bank of England) will have to both raise interest rates and wind down their asset purchase programs. This is a difficult endeavor at any time, made more precarious in today’s world of stagnant global demand, minimal wage growth, and stubbornly low inflation. In spite of this, we remain optimistic that the Fed will soon embark on a slow but methodical tightening of monetary conditions that will result in capital market volatility, but will not upend the global economy in the near term. “Optimistic”, but far from certain.

Problem #2: Clear Communication

A key element to normalizing monetary policy is setting the right expectations. Tell the market what you’re going to do and then do it. If consumers, businesses, and investors see it coming and understand the rationale, economic dislocations can be minimized. While Chair Janet Yellen and her predecessor, Ben Bernanke, have championed the idea of greater transparency through forward guidance and other communication tools, the message has become a bit more muddled lately.

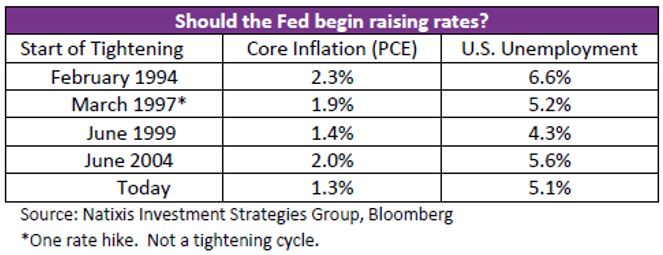

The Fed’s dual mandate of price stability and full employment should make policy decisions fairly straightforward. Prior to the September FOMC meeting, this scorecard appeared clear:

1)At 5.1% unemployment, the U.S. economy appearsto be at or close to full employment, and

2)Core inflation measures year-over-year (PersonalConsumption Expenditures (CPE) Price Index andConsumer Price Index (CPI)) were below the Fed’s 2% target, but are expected to rise toward thattarget as unemployment falls.

In summary, the dual mandate should have implied a Fed on the verge of tightening – holding back only because inflation is a bit too low. However, the message of September’s meeting was derailed by talk of “Recent global economic and financial developments” – i.e., China’s slowing economy and its impact on emerging markets. Did the Fed throw a monkey wrench into its dual mandate?

To be fair, the September FOMC statement highlighted global economic developments in terms of putting “further downward pressure on inflation in the near term.” A technical interpretation would be that the Fed was still operating within its dual mandate. But that message was far less clear to investors. Had the Fed added “global economic developments” as another variable? There is no forward guidance for a slowing global economy. How would it be measured? How much would or could it alter the Fed’s plans? As evidence of this confusion, stocks oscillated wildly in the hours after the announcement. Moreover, while holding the line on rate hikes should have been perceived as bullish, the S&P 500® lost 5.7% and fell in seven of the next eight trading sessions. The Fed does not have a communication problem yet, but it is on the verge of having a communication problem if it continues to highlight amorphous “global developments.”

Problem #3: Maintaining Credibility

Beyond the uncertainty of global markets, the Fed may soon have to address every central banker’s nemesis – inflation. Given known demographics and labor force participation trends in the U.S., even modest economic growth is likely to continue pushing the unemployment rate lower, below 5%. Having seen no evidence that inflation has decoupled from unemployment (i.e., the Phillips Curve), the Fed has to decide how low unemployment can go before it falls “behind the curve.” While the Fed would like some inflation, it cannot let inflation expectations become untethered or it will lose credibility. A central bank without credibility will not be able to effectively manage interest rates or credit creation. Moreover, aggressively raising rates to regain credibility would likely constrain growth further and create unnecessary volatility in markets. The Fed does not have a credibility problem yet, but it is on the verge of having a credibility problem if unemployment falls below 5% without a rate hike.

An Equity Collar?

Since late 2014, we have grown more cautious on global equity investing. However, we remain neither excessively optimistic nor pessimistic. In many ways, the payoff to stocks looks similar to “equity collar” – a strategy that leaves little room for large gains or losses.

Limited Upside

Over the intermediate term, two factors are to likely limit capital gains for stocks. First, the forward P/E ratio for the S&P 500 is approximately 17.0x. That level represents valuations that are elevated but not excessive, given low interest rates. Across both developed and emerging markets, P/E ratios show a similar pattern. As we have noted before, stocks are not overvalued (implying that their P/Es should fall), but they are “fairly valued” (implying that their P/Es shouldn’t rise). Eventual Fed tightening also makes P/E expansion all the less likely.

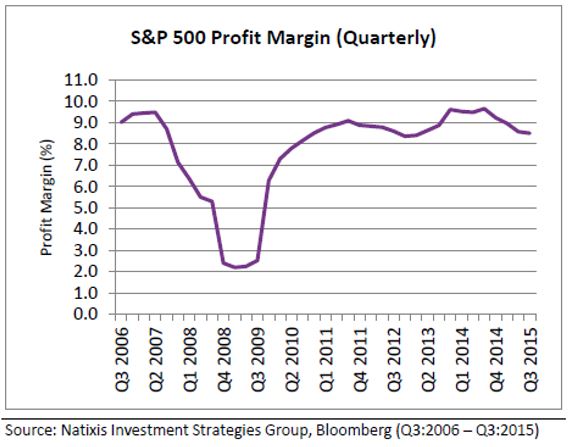

Second, earnings growth may be positive, but will remain sub-par. At close to 10%, U.S. corporate profit margins remain near cyclical highs. They are also unlikely to expand from this level. Without margin improvement, earnings growth cannot deviate too far from nominal GDP, which across much of the developed world is between 0% - 4%. Earnings growth for the S&P 500 will likely be flat for 2015. Earnings may improve somewhat in 2016 as profits in the energy sector stabilize, but the effect will be modest as the energy weighting accounts for only 7% in the S&P 500 and 5% in the MSCI EAFE Index. Share buybacks remain in vogue, but they are hardly the magic elixir for per share earnings growth they once were when stocks were cheap. While most of the damage to U.S. earnings from a stronger dollar has been done, a tailwind from a weaker dollar is unlikely. In summary, earnings growth is likely to be positive, but modest.

Our risk scenarios (defined as unlikely, but plausible) to the upside include stronger earnings growth from the energy windfall (see below) or a strong rebound in Chinese and emerging market growth.

Our risk scenarios (defined as unlikely, but plausible) to the upside include stronger earnings growth from the energy windfall (see below) or a strong rebound in Chinese and emerging market growth.

Limited Downside

While we see only limited upside for stocks (modest earnings growth + a 2% dividend on the S&P 500), we also view a U.S. bear market as unlikely. One, forward looking indicators such as the U.S. ISM Composite and Leading Economic Indicators (LEI) imply that a recession in the near term is unlikely. Two, the U.S. Treasury yield curve remains upwardly sloping, implying favorable credit conditions. Three, the cost of gasoline and heating oil have declined significantly in the last year, and those savings will eventually end up in consumers’ pockets. Four, housing, construction, and auto manufacturing/sales appear to be strong and the U.S. service economy continues to expand solidly (although the much smaller manufacturing sector continues to struggle). These are hardly the hallmarks of a recession or bear market.

Our risk scenarios to the downside include a Fed policy mistake, a decline in profit margins, or further unanticipated slowing in China or a bursting of their debt bubble.

The eventual onset of Fed tightening, along with the unknowns associated with China’s slowdown, are likely sources of more short-term volatility in global equities. That volatility is likely to be rewarded with positive, but below-average equity returns over the next few years.