Credit spreads widened sharply in March as investors reallocated from higher risk assets to safer ones. Companies struggled to access bond markets as a result. [1] Credit-rating agencies have also downgraded many companies as more countries have gone into lockdown, hurting all borrowers, and weaker ones in particular. [2]

At the same time, the speed and scale of combined policy responses by governments and central banks have been unprecedented. The vulnerabilities in the high-yield market – highlighted by negative total returns seen in March [3] – could be somewhat offset by the crisis response measures. Although there can be no guarantees, particularly given the uncertainty over the duration of this health crisis and the economic shock it has triggered, investors may look back on this period as an attractive entry point into high yield.

What vulnerabilities has the spread of COVID-19 highlighted in the market?

The greatest downside risk for high yield is the risk of recession, and this is what the near term holds. In this context, companies are not overly leveraged compared to levels seen at the start of previous recessions – for example, debt levels up to six times EBITDA (Earnings before interest, tax, depreciation and amortisation) that were typical before the global financial crisis.

However, given the sudden and sharp contraction in economic activity, even current debt levels – of around four times EBITDA – are enough to create financial difficulties and defaults for high-yield issuers (Source: BofA Merrill Lynch, as of March 31, 2020).

Has this crisis thrown up any particular surprises?

The fact that everything but essential goods and services has pretty much shut down is extraordinary. Against the backdrop of lockdowns and containment measures, which no one could have expected a few weeks ago, it is not really a surprise that businesses have not had time to adapt their cost structures and are taking a significant hit to profits.

Has the dislocation in the high-yield market been indiscriminate, or are investors discerning between the fundamental qualities of businesses?

Selling has been indiscriminate so far. With exchange-traded funds forced to sell bonds due to large outflows, the sell-off has occurred across the board, with no meaningful marginal buyer on the other side of the trade. [4] As liquidity has dried up, investors have been selling what they can rather than what they would like to.

What does it mean in terms of default and downgrade risks?

At current yield levels, our view is that long-term investors are being overly compensated for default risk because, although defaults are expected to rise across many sectors, that risk is already more than priced in. For instance, current spreads in US high yield imply a five-year cumulative default rate of about 40 per cent. Meanwhile, European high yield is currently pricing in a default rate of around 35 per cent, assuming the worst (i.e. zero recovery rates). By way of context, the highest historical global five-year cumulative default rate was 32 per cent. [5]

In terms of downgrade risk, widespread containment measures have resulted in downgrades outnumbering upgrades – a period of ‘negative ratings migration’ to use investment parlance. B-rated companies being downgraded to CCC in particular look as if the negative-rating trend has not necessarily been priced in yet.

With CCC spreads at over 1,400 basis points as of 13 April, [6] B-rated bonds downgraded to CCC should start pricing in a higher risk of default and see spreads widen.

At the other end of the high yield credit-rating spectrum, the US Federal Reserve’s (Fed) recent move to broaden its mandate and buy recent and future fallen angels may help BB spreads to compress. By the end of March, a few large companies had been downgraded to high yield (i.e. had become fallen angels), totalling around $150 billion of debt over the first quarter, including household names such as Ford and Macy’s. [7] While we expect a record amount of debt to be downgraded from investment grade to high yield, the Fed’s buying programme should offer meaningful support for the higher-quality end of US high yield.

Where might investment opportunities emerge?

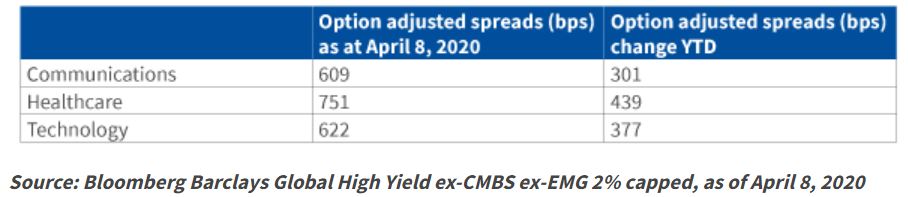

In the near term, companies in defensive sectors such as telecoms, healthcare and selective areas of technology look attractive, having been heavily sold relative to the fundamental strength of their businesses (Figure 1).

Figure 1: Spread changes January to April 2020 in selected sectors

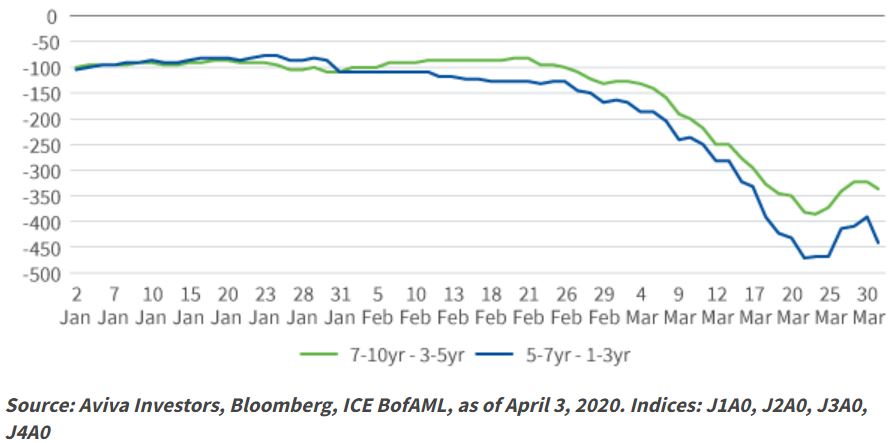

The recent dislocation means many high-yield issuers’ credit curves are now fairly flat, or in some cases inverted (Figure 2). Therefore, on a case by case basis, shorter-dated securities can offer attractive opportunities where a company has ample liquidity and analysis shows low default risk.

Figure 2: Example of curve inversion in US high yield

How do you gauge the impact of the policy response to date?

Support from central banks and governments’ fiscal responses will play a crucial role in limiting the extent and duration of the downturn.

In addition to fallen angels, the Fed has also included high yield ETFs on the list of eligible instruments it can buy. While purchases may be small in the grand scheme of things, they signal the bank’s willingness to provide support to US corporates of lower credit quality.

Many other governments have also taken action, and their crisis-response measures are helping borrowers deal with the credit crunch through aid such as loans, tax relief and contributions to labour costs. Unfortunately, even the generous amounts pledged by governments and central banks will not be enough to support all the companies in the high yield sector. Issuer selection will therefore be critical – for instance identifying companies that provide important goods or services, and those that are large employers. These are the most likely to be supported throughout the period of restrictions.

Will the re-pricing of risk be short term?

A lot of bad news has already been priced into high yield, providing attractive spreads and yields for investors wanting to take or add exposure to the asset class, although spreads could widen further in the short term if lockdown and containment measures are prolonged. COVID-19 has led countries, economies and financial markets into uncharted territory, and uncertainty remains high. However, if restrictions can be lifted in the next few months, given levels of government support, we expect markets to recover a large part of the losses and spreads to meaningfully tighten again over the next 12 months.