In recent weeks, market conditions switched swiftly from panic mode to exuberance mode. Active investors are scratching their heads as markets no longer seem to be discounting a U.S. recession and any Fed rate hike in 2019.

In our view, the January rally is a good reason to gradually reduce risk in portfolios, especially in Europe where the probability of a hard Brexit has increased. Concurrently, the U.S. equity market rebound was led by value stocks, which seems unsustainable. Yet, any aggressive de-risking seems premature as a U.S. recession risk is contained.

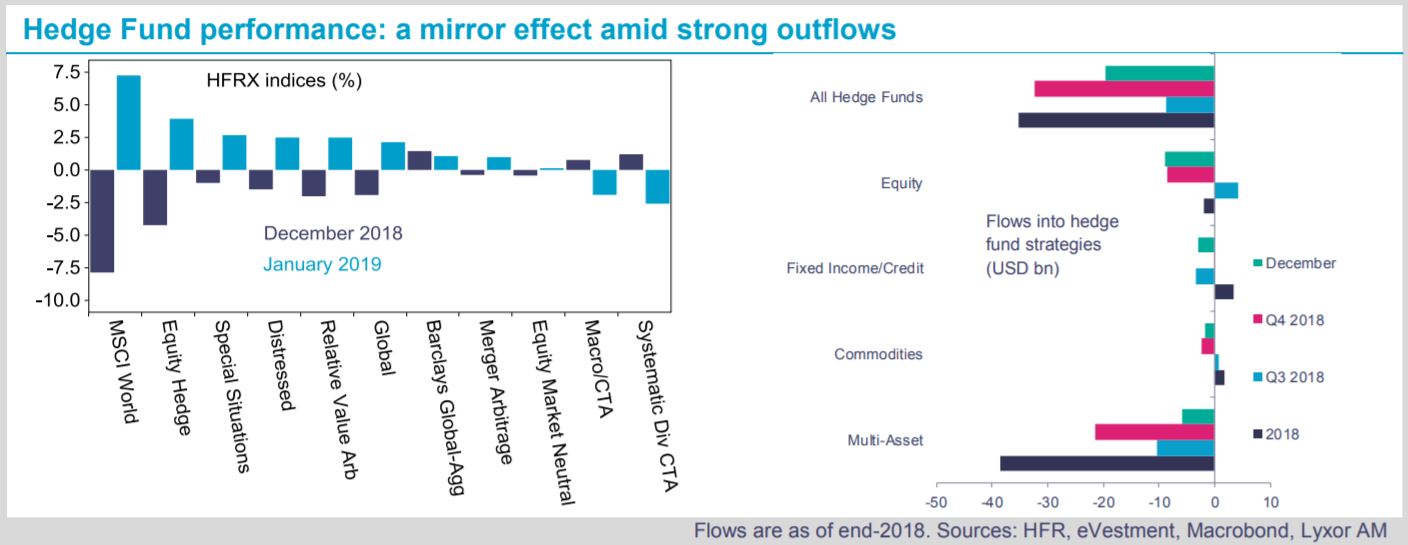

In the meantime, hedge fund strategies experienced a symmetric move. The strategies that suffered in December rebounded last month (L/S Equity, Relative Value Arbitrage), while those resilient at the end of 2018 (CTAs) lagged behind. Looking at performance over the past two months, Event-Driven stands out as the outperforming strategy and Macro/ CTAs as the underperforming one, according to broad benchmarks.

CTAs suffered from the trend reversal in equities at the turn of the year, down 2.6% in January after a dismal year in 2018. Their long positioning on bonds is now at risk if improved economic expectations eventually translate into higher bond yields, as we expect.

What does this mean in terms of strategic allocation? First, we still prefer strategies that were resilient in recent downturns and didn’t suffer during the rebound. This includes Merger Arbitrage and Fixed Income Arbitrage and to a lesser extent L/S Equity Market Neutral and Global Macro. Second, we stay cautious on L/S Equity strategies with an elevated net market exposure and prefer flexible L/S Equity strategies that can adjust their beta according to market conditions. Third, the outlook on Emerging Market (“EM”) assets has improved since the Fed has turned less hawkish. EM-focused Global Macro strategies could benefit from it. We thus have a bias in favour of Global Macro vs. CTAs.

The latter tends to suffer when markets experience such gyrations, but CTAs should protect portfolios if things go wrong and a persistent downward trend in risk assets eventually takes shape. Overall, we continue to believe that alternative strategies are attractive relative to traditional assets at this stage of the business cycle. However, caution is required on strategies with a long equity market bias and selectivity is key from both a top-down and bottom-up perspective.