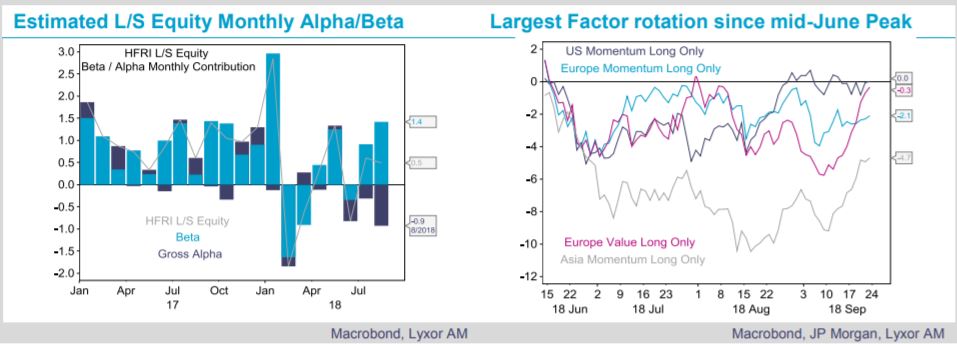

L/S Equity strategies were the primary culprits and victims. In the U.S., managers had steadily reduced their overall net exposure and leverage since Q2. As a result, they partially missed the summer rally. The plunge in Momentum in June was also costly, only partially recovering afterward. Stock selection in their heavyweight tech, healthcare and cons. discretionary sectors didn’t help enough. In Europe, strategies adequately reduced their overall exposures ahead of the summer.

Unfortunately, many strategies were too early in chasing Value stocks, which continued to correct.

In Asia, strategies had also turned cautious before the summer. However, they were caught in their long tech and Chinese positions, which strongly underperformed main markets.

Within the L/S Equity space, neutral strategies also suffered. In addition to the major swings in Momentum in the U.S. and in Asia, and in Value in Europe, most other factors were volatile, which steadily eroded their returns. Finally, many managers reported elevated hedging cost as one notable factor, amid declining volatility in developed markets.

Meanwhile, the diversification from CTAs and Merger Arbitrage was of little help this time. Both strategies were flat or so. CTAs navigated a lack of trends in most segments, to the notable exception of EM assets.

The tightening in deal spreads before the summer left limited leeway for Merger managers to extract substantial returns. The positions in Special Situation portfolios did generate some alpha overall, but more than offset by their costly long beta exposure. Fixed Income Arbitrage strategies remained isolated but remained overall flat.

In our view, the difficult summer for hedge funds in general, and for L/S Equity, largely results from one central cause: worldwide policy uncertainty.

The shifts in trade expectations, vulnerable progresses in Italy and UK, the anti-establishment push in a number of DM and EM countries, the intensifying use of economic sanctions all keep markets in feverish stance, with limited source of uncorrelated returns. It prevents managers from deploying their strategy successfully. Some light might return before year-end.