As we go to press, it looks likely that Democrats will also run the Senate, in addition to the White House and the House of Representatives. With expectations that this will translate into greater fiscal stimulus in the near-term, bond yields moved upwards in the U.S. and the Treasury curve steepened. European rates were also under pressure, though the surge in yields was more limited there. Considering the current level of bond yields, the upside potential is huge under a Democratic sweep and would have global reverberations across countries and asset classes.

In our view, Covid-19 headwinds and Fed bond purchases should contribute towards containing any substantial rise in yields in the near term. In the longer term, structural factors such as demographics and technology advances should also prevent a normalization in yields to levels seen before the Global Financial Crisis. Yet, we will probably converge in the next couple of years to the range of 2 to 3% last observed in 2017-2018. How fast we will get there is what matters for markets at this critical juncture. Our base case assumes we will not get there in H1-2021.

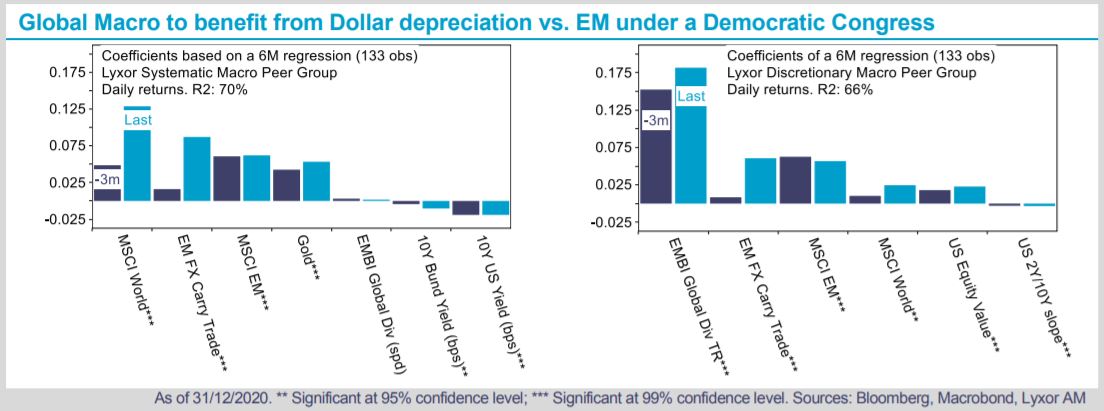

In the space of alternatives, Global Macro strategies appear interesting to play this partial and back ended normalization in bond yields. Their long position on fixed income has been reduced lately and, in some cases, turned slightly short on Treasuries. Inflation linked bonds and EM bonds now represent the bulk of the fixed income exposure. Discretionary strategies also appear to have reduced their sensitivity to a steepening of the Treasury curve. Meanwhile, their short USD bias in FX could also be rewarded under a Democratic Congress with twin deficits pushing the USD lower. The worst-case scenario, whose probability is low, would be a brutal rise in yields that would derail equities, lifting the USD and hurting EM assets. Under that scenario of a sharp trend reversal across asset classes, Global Macro strategies still have the potential to outperform other hedge fund strategies, in our view. Our stance thus remains Overweight.