For an investor, investing in growth stocks can be a particularly wise choice over the long term. But it can also be a useful tactic within a portfolio diversification strategy, particularly if the companies adhere to certain ethical criteria. This responsible investment dimension gives fund managers and investors the opportunity to review their approach and analyse recent innovations, such as the index described in this article, which are not only financially robust but can also offer extra-financial benefits.

A relevant choice for investors

In an article written in 1958, "Common Stocks and Uncommon Profits", Philip Fisher laid the foundations for investing in growth stocks. He suggested that investors target growth-oriented companies, with high profit margins, high return on capital, a commitment to research and development, a well above average sales organisation, industry leadership and exclusive products or services.

More recently, an article entitled "Style timing Value vs. Growth” in the Journal of Portfolio Management [1], explains that technological disruptions and even the phenomenon of globalisation have enabled growth companies to increase their profits over the long term, to a much greater extent than the average for their sector. Historically, profit growth has been one of the key factors in the performance of companies on the stock market.

The integration of extra-financial criteria

A study published in July 2020 by BNP Paribas Asset Management reveals that extra-financial ESG (Environment, Social and Governance) criteria have increased in importance for 23% of investors since the Covid pandemic, even though 81% of them were already applying ESG criteria in some or all of their portfolio management and 16% were planning to do so before the crisis [2].

Investing over the long term in growth stocks which meet high ESG standards limits the effects of potential reputational issues. This is also the case when using a quantitative investment approach.

BNP Paribas Growth Europe ESG Index

Investors can now dovetail the theme of European growth stocks with that of ESG by choosing to invest in an exchange-traded fund (ETF), EGRO FP Equity, which replicates the BNP Paribas Growth Europe ESG Index (Bloomberg: BNPIFEGE Index). This became listed on the stock exchange on 22 June 2021.

Its initial investment universe is all stocks listed in Europe with an average daily trading volume of over EUR 10 million on a monthly basis over the last six months. These are then put through a second filter, taking into account ESG exclusion factors and data on each company’s carbon footprint. In this way, at least 20% of the companies in the investment universe are excluded through innovative filters, such as taking into account, potentially on a daily basis, any controversies reported by the data provider. The next filter maximises the ESG score and growth factors. Stocks are scored on four weakly correlated metrics that best represent the growth factor:

- Capex growth over five years (capital expenditure specifically on the purchase of equipment)

- Internal growth rate

- Five-year growth in the number of employees

- Anticipated sales growth over one year.

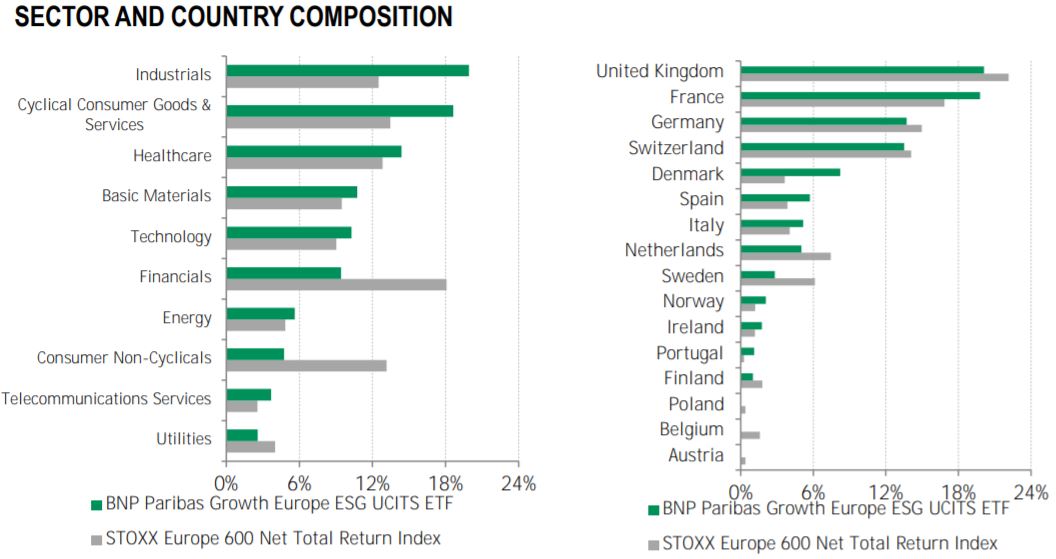

These growth companies are then weighted to achieve good diversification while taking into account their market capitalisation. The BNP Paribas Growth Europe ESG index investment selection is also more concentrated than the Stoxx® Europe 600 index mentioned below, with approximately 70 stocks in the portfolio.

In addition, the BNP Paribas Growth Europe ESG index must comply with certain constraints in relation to the initial investment universe:

- Any deviation from the risk budget is limited to 4% per year

- Any deviation in the weight of any sector is limited to 10%.

- A lower carbon footprint

- A higher ESG score.

Finally, the BNP Paribas Growth Europe ESG index currently favours the healthcare sector, new technologies and luxury sectors. It thus includes overweighted companies such as Dassault Systèmes (1.2% vs. 0.3% for the benchmark) and Hermès (2% vs. 0.4%). The financials sector is underweighted but includes some of the most innovative companies, such as Euronext for example.

- Source: BNP Paribas as of 31May 2021. Past performance is not a reliable indicator of future returns. Comparative index: STOXX Europe 600 index, Bloomberg code:

. Comparative index for illustrative purpose only.

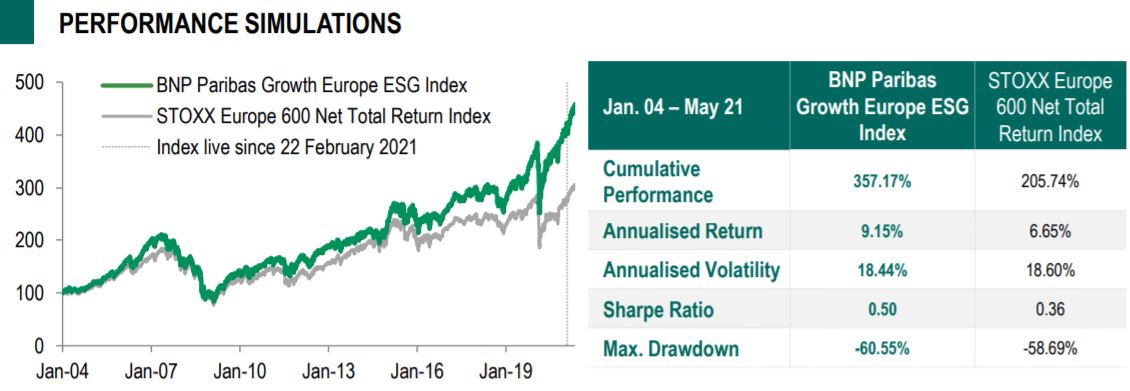

In terms of performance, from its creation in 2004 up to the end of May 2021, the BNP Paribas Growth Europe ESG Index has gained 14.08%, with an annualised volatility of 18.44% and a Sharpe ratio of 0.50 (simulated data). These figures are better than the benchmark index in this article, the Stoxx® Europe 600 index, which gained only 13.46% for a higher risk level over the same period (18.60%).

- Source: BNP Paribas and Bloomberg as of 31 May 2021. Performance simulations of the BNP Paribas Growth Europe ESG Index are Total Return and in EUR, net of

0.30% fees p.a, from 27 January 2004 until 21 February 2021, historical data thereafter. Historical performance on

from 27 January 2004. Past or simulated performance or achievement is not indicative of current or future performance. Comparative index for illustrative purpose only. This is for general information only and should not be used as a basis for making any specific investment, business or commercial decisions. Any economic and market trend, prediction, projection or forecast is not necessarily indicative of the future or likely performance of the funds.

The investment theme of European growth stocks is very much in vogue at the moment, despite the emphasis over the last six months on portfolio rotation towards value stocks. However, while this rotation is well underway in the US, both in terms of market sentiment and valuation, the situation is somewhat different in Europe, where many investors like European growth companies, for three main reasons:

- There is strong growth in private equity and venture capital fundraising, now heightened by the current political and economic drive to revive European growth champions.

- There is greater diversification across European growth companies than in the US, where technology stocks dominate allocations despite being very expensive in terms of their average price-to-earnings ratio.

- The likely trajectory of interest rates differs in Europe, where low rates are expected to remain around their current levels for longer than in the US. This is an important macroeconomic factor in the valuation of high growth companies.