During the first quarter of 2016, hedge funds suffered a 2% drawdown according to the Lyxor Hedge Fund index. Across hedge fund strategies, CTAs and Merger Arbitrage have been the only segments of the industry being able to post returns in positive territory in Q1. Meanwhile, L/S Equity underperformed as a result of the tough market conditions and the sharp rotation in risk factors which saw a strong but short lived rebound in value stocks.

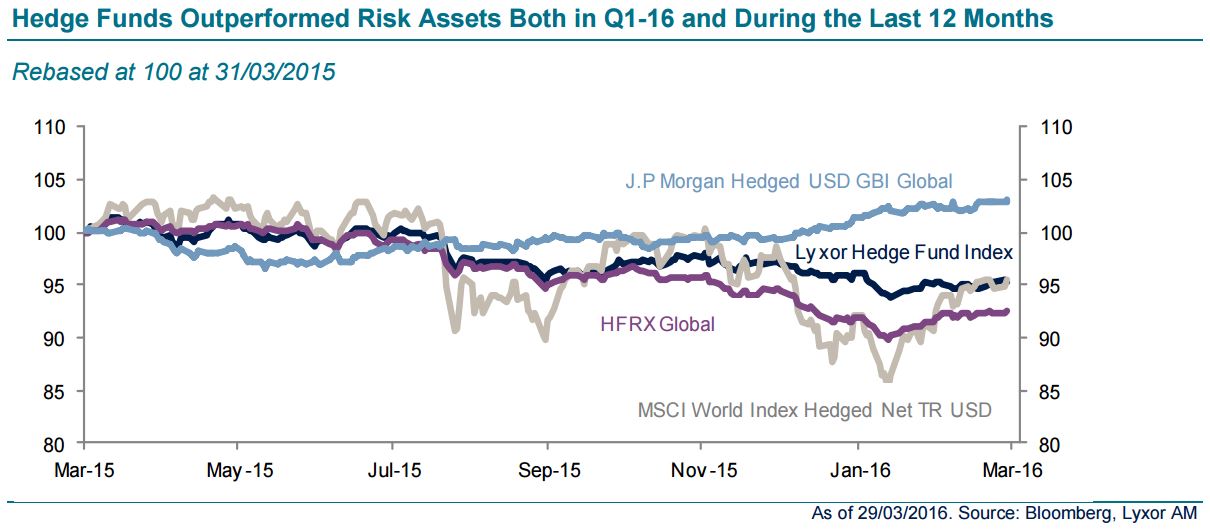

In this environment, the hedge fund industry has been criticized for delivering disappointing returns. However, the performance of hedge funds must be evaluated in relative terms (see chart). The turbulent market conditions over the last twelve months saw the MSCI World down almost 5%, with the Stoxx Europe 600 and the Topix 100 down by 12% (in TR and local currency). Government bonds continued to edge higher, but valuations are so stretched that it seems ill advised to dig further into the asset class at present.

Hedge funds are down by 5% over the last twelve months according to our measure, but the volatility of their returns is divided by three compared to equities. The annualized volatility of the Lyxor Hedge Fund index is 5% over the last twelve months, compared to 15% for the MSCI World.

As a result, on a risk adjusted basis, hedge funds have fared much better than risk assets both in Q1 and over the last twelve months.

With regards to the most recent period, March saw a revival of L/S Credit strategies (which we upgraded early March).

Merger Arbitrage also delivered healthy returns in March after showing strong resilience in January and February. We recently reaffirmed our overweight stance on Merger Arbitrage. Meanwhile, CTAs are down in March to the extent that their defensive positioning (long fixed income, neutral equities, short energy and long JPYUSD) suffered during the market rebound.

But dovish central bankers provided a floor to their long fixed income positions and limited the losses of the strategy. We remain neutral on CTAs for the time being.