As a result, expanding valuation multiples will no longer push stocks higher; instead stocks must rely on actual earnings growth.

In a market where there will be a wide disparity between winning and losing stocks, only intensive research will uncover the likely winners. That means engaging with company managements to understand their competitive positions and how they will be affected by 2022’s major economic themes.

We think there are three themes that matter at the beginning of what is likely to be a bumpy year. As we move towards recovery from the Covid-19 pandemic, even though this will not be a linear path, understanding how individual companies and their business models will fare given the prevailing macro environment and these major themes will give investors an edge.

Theme 1: Products versus services

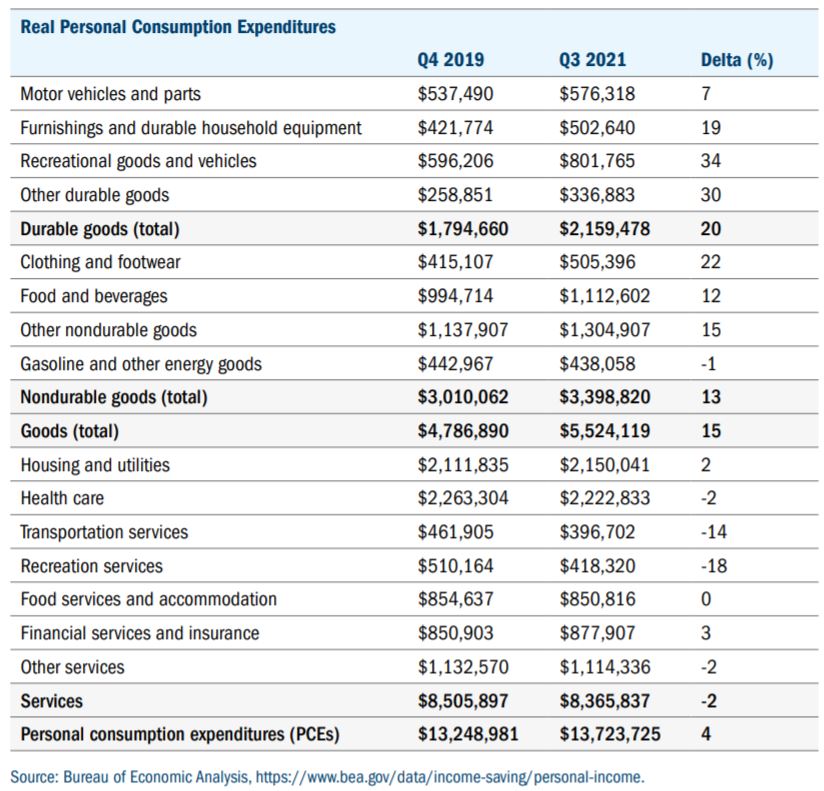

Firstly, there is the question of how consumers will expend pent-up demand. Before the pandemic, consumers preferred “experiences”. As a result services such as travel, hotels, restaurants, flights and cruises were in hot demand. But social distancing turned that on its head, with the result that US consumer spending on goods such as furnishings and clothing is up 21% since the end of 2019, yet spending on services languishes at pre-pandemic levels [1].

As 2022 progresses, the pandemic’s likely retreat will favour services once more. But to what extent? And will the Omicron and Delta variants slow the reversal?

Figure 1: Goods demand outstrips services

Theme 2: Continuing shortages

A related theme is the shortages beleaguering the economy and stoking inflation. They predominantly affect three areas: retail inventories, the supply chain and labour. To start with, retail inventories are struggling to keep up with consumer demand for goods – such lean inventory is restraining sales. Supply chains, too, are having a hard time keeping up, gridlocked by factors such as a resurgence in demand and bad forecasting. We think that supply chain shortages will ease in early 2022 and stabilise over the course of the year, probably returning to normal by the beginning of 2023. In terms of labour, there are still four million missing workers due to a combination of Covid-19 deaths, early retirement, caregivers not returning to work and lower levels of immigration.

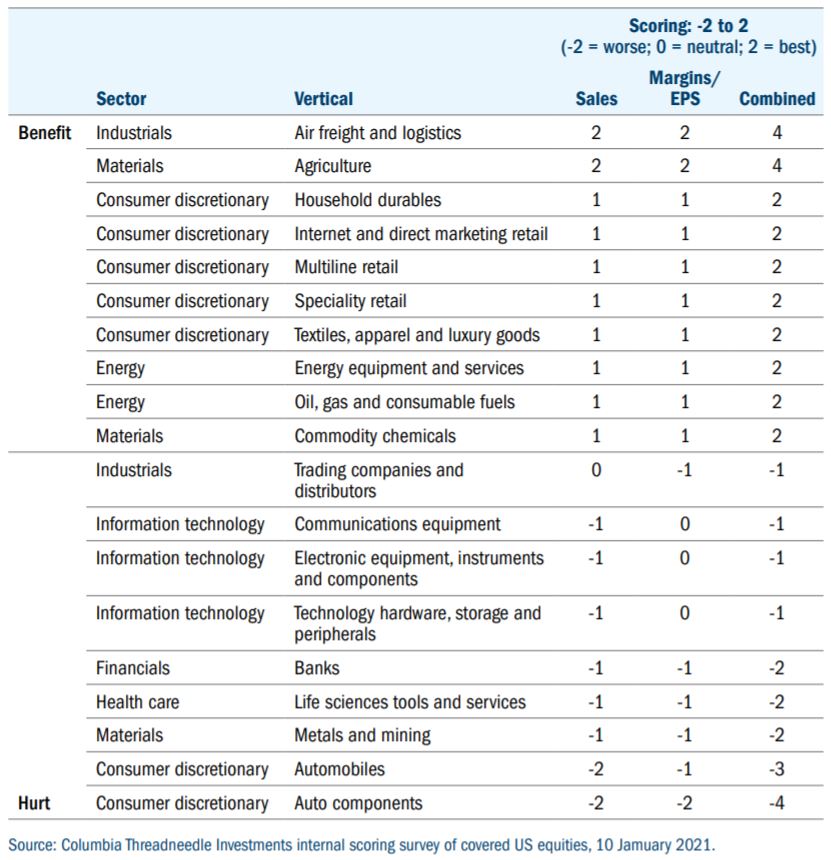

Perhaps counterintuitively, shortages benefit some companies because they bolster pricing. Our analysts judge that businesses in areas such as air freight and agriculture have most to gain from shortages, while automobile companies, miners and even banks have much to lose.

Figure 2: Who will be the winners and losers from 2022’s shortages?

Theme 3: ESG’s rise

A longer-term theme set to accelerate in 2022 is consumer concern about climate change. North American companies are already starting to respond by changing their behaviour; expect the pace to pick up next year. For instance, Union Pacific, North America’s biggest railroad company, published its first climate action plan at the end of 20212 detailing steps to reduce its environmental impact, with an eye to achieving net-zero emissions by 2050. Others will follow.

We are engaging with companies in a consultative manner about environmental, social and governance (ESG) issues, seeking to understand what they are doing, as well as how this may impact their earnings over time.

Conclusion: Rewarding research intensity

2022 will be a year when the Federal Reserve tightens monetary stimulus for the first time since the 2009 global financial crisis. In many ways, this will mark a watershed. Tighter monetary conditions will make equity markets more discriminating as higher earnings become the main driver of stock price gains.

In such a changed environment, progress for equities will be bumpy and uneven. Intensive research will be needed to find the stocks able to continue growing their earnings.